Parametric Insurance: A Powerful Tool for Energy Companies Facing Natural Catastrophe Risk

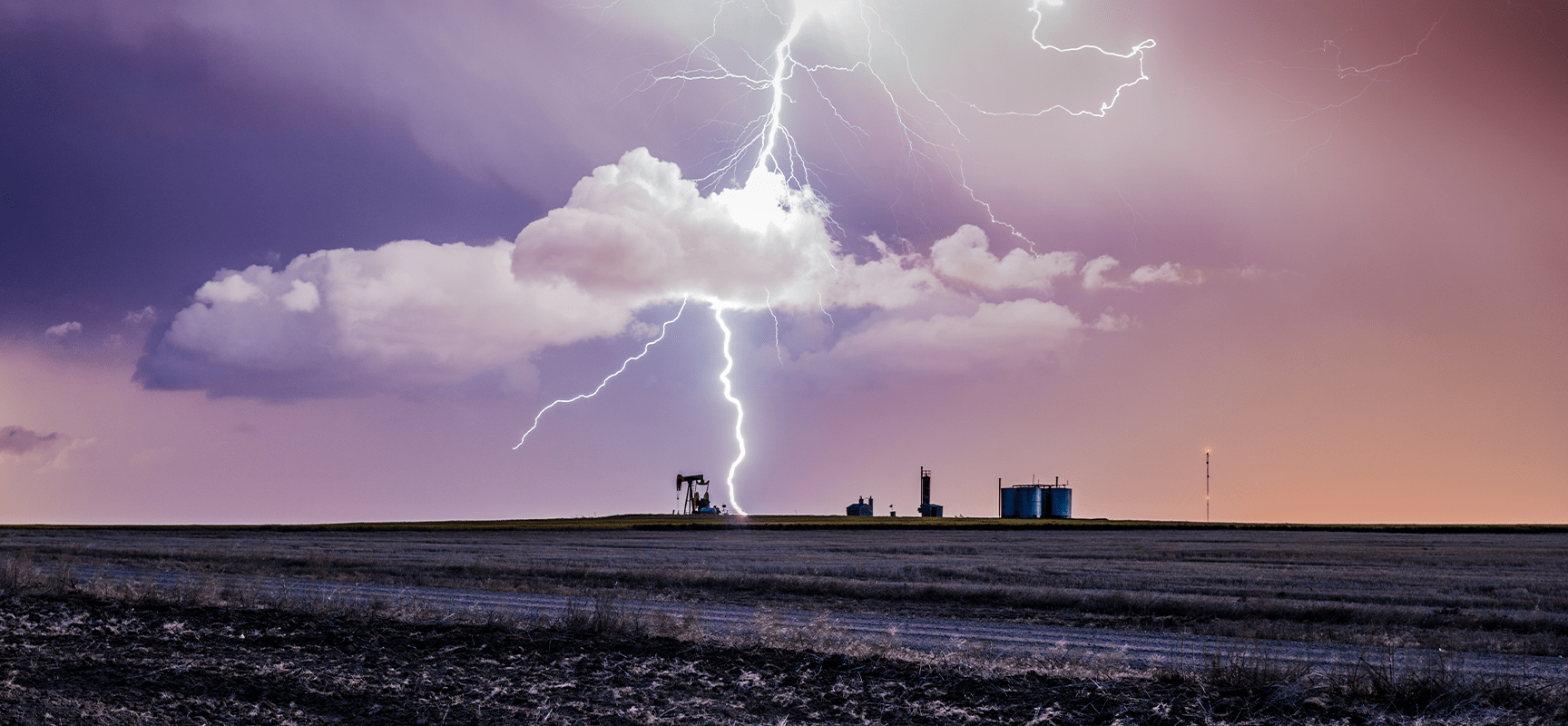

Energy companies face unique challenges when it comes to insuring against natural catastrophes. Hurricanes, wildfires, hail, tornadoes, earthquakes, and floods can cause widespread disruption to operations and significant financial losses. Traditional property policies help, but deductibles, exclusions, and sub-limits often leave costly gaps.

That’s where parametric insurance comes in.

Every energy company’s exposures are different. Let’s design a program that works for you. Connect with our Energy team to learn more.

What is Parametric Insurance?

Unlike traditional insurance, which pays after a claim’s adjustment process, parametric insurance pays when a pre-agreed parameter is met. The trigger could be wind speed, hail size, flood depth, wildfire spread, or seismic activity.

For example:

- If a hurricane of a certain strength passes within a set distance of a refinery, a payment is issued.

- If hail larger than a specified size impacts a solar farm, funds are released.

- If an earthquake exceeds a defined level of ground acceleration, the policy pays out.

Payments are typically made within 14 to 21 days, much faster than traditional claims.

Why Energy Companies are Exploring Parametric Coverage

Energy companies often operate in catastrophe-prone regions, with infrastructure that is highly exposed. Parametric insurance offers several advantages:

- Speed and transparency: Claims are verified by independent data sources such as NOAA or USGS, removing disputes and delays.

- Flexibility of funds: Payments act as a “bucket of cash.” Unlike traditional property policies, there are no sub-limits or restrictions. Proceeds can be applied to repairs, debris removal, overtime pay, employee relocation, or even loss of tax credits.

- Closing protection gaps: Parametric insurance can sit above deductibles, fill in for sub-limits, or cover exposures not insured elsewhere.

- Customization: Each policy is built around specific risks and pain points, whether it’s hail-resistant solar panels, wildfire liability from transmission networks, or temperature swings impacting power generation.

- Minimizing basis risk: Programs are collaboratively designed with the broker, client, and carrier to align payouts as closely as possible with potential losses.

Examples in the Energy Sector

- Solar farms: Protection against hail and tornadoes, tailored to panel durability and stow systems. Some structures can even address potential losses of solar investment tax credits.

- Refineries and pipelines: Coverage for hurricane, flood, or earthquake triggers that could impact operations.

- Transmission and distribution networks: Options to address wildfire risk and related liabilities.

- Data centers and utilities: Heat index or temperature-based coverage to protect against outages, equipment strain, or higher energy costs.

- Flood-exposed sites: Sensor-based coverage that measures water depth on-site and triggers payments quickly.

Is Parametric Insurance Right for You?

Parametric coverage is not meant to replace traditional insurance, but to complement it. Think of it as a scalpel, not a sledgehammer. It works best when:

- There is a clearly defined risk that can be measured by reliable data.

- The organization wants to reduce volatility tied to deductibles, sub-limits, or exclusions.

- Rapid access to capital after an event is critical to business continuity.

As natural catastrophes continue to impact the energy sector, parametric insurance offers a data-driven, transparent, and efficient way to protect against losses. It allows energy companies to recover faster, allocate funds where they are needed most, and build greater resilience into their operations.

Related articles

In New Mexico, proposed changes to the plugging and abandonment (“P&A”) bonding requirements are a hot topic across the oil and gas industry. While these changes may be intended to reduce the number...

The Occupational Safety and Health Administration (OSHA) sets the standards for ensuring safe and healthful working conditions across the United States. But when an OSHA citation lands on your desk,...

Texas is unusual in that most private employers can choose not to participate in the state's workers' compensation system. These employers are called non-subscribers. Since they operate outside the...